Picture this. It’s the 5th of the month. Your salary just hit your account, and before you’ve even had your morning chai, rent, groceries, phone bills, and a weekend trip with friends have already claimed most of it. By the 25th, you’re watching your balance and wondering where it all went.

If that sounds uncomfortably familiar, you’re not alone. Most people in their mid-20s earning around ₹30,000 a month feel like investing is something they’ll do “later” — when they earn more, when life settles down, when the timing feels right. But here’s the thing nobody tells you: waiting is the most expensive financial decision you’ll ever make.

The amount you invest matters far less than when you start. Even ₹3,000 a month, started today, can do what ₹10,000 a month started at 35 cannot. This guide will walk you through exactly how to start investing with a ₹30,000 salary — no confusing terms, no generic advice, just a practical plan you can actually follow.

What’s the Best Way to Start Investing with a ₹30,000 Salary?

Quick Answer: Build an emergency fund of 3 to 6 months of expenses first (roughly ₹60,000 to ₹90,000) in a liquid savings account. Then invest ₹5,000 to ₹6,000 every month through SIPs in index funds and diversified mutual funds, with a small portion going into PPF for tax savings. Use the 50/30/20 rule to guide your budget: 50% for needs, 30% for wants, and 20% for saving and investing.

Why Starting at 25 Is a Bigger Deal Than You Think

Time Is the Ingredient Money Can’t Buy

Let’s talk numbers, because they tell a story better than any motivational quote.

Say you invest just ₹5,000 per month starting at age 25, earning an average annual return of 12% (which is roughly what diversified equity mutual funds have historically returned in India over long periods). By the time you’re 55, you’ll have accumulated approximately ₹1.76 crore — from a total investment of just ₹18 lakh. That’s your money multiplying nearly 10 times.

Now imagine you wait until 35 to start. Same ₹5,000 per month, same 12% returns. At 55, you’d have around ₹50 lakh. You’d still be investing for 20 years. But you’d be walking away with ₹1.26 crore less.

That difference isn’t discipline. It isn’t luck. It’s compounding — the process by which your returns earn their own returns, growing your wealth exponentially over time. The longer compounding has to work, the more dramatic the results. Warren Buffett, arguably the world’s greatest investor, earned more than 99% of his wealth after his 50th birthday — not because he suddenly became smarter, but because his earlier investments had been compounding for decades.

Inflation Is Quietly Shrinking Your Savings Right Now

This one stings a little. India’s inflation has averaged around 5 to 6% per year. If your money sits in a regular savings account earning 3 to 4% interest, you are technically losing purchasing power every single year. That ₹10,000 you save today will buy less in 5 years than it does today.

Equity mutual funds and index funds have historically delivered 10 to 14% annual returns over long periods. That’s not just beating inflation — it’s lapping it. Financial planning, at its core, is making sure your money grows faster than prices rise.

Build Your Emergency Fund Before Anything Else

This is the step most people skip, and it’s the one that undoes everything.

Imagine you’ve been disciplined for 18 months, building a nice little SIP portfolio. Then your bike gives up, your company does layoffs, or a family member needs hospital care. Without a financial cushion, you’re forced to withdraw your investments — often at the worst possible time, when markets are down — and lock in a loss. All that discipline, gone.

An emergency fund is your financial shock absorber. It lets you keep your investments intact, no matter what life throws at you.

How much should you save? Aim for 3 to 6 months of your monthly expenses. If you spend around ₹18,000 to ₹20,000 per month, your target is roughly ₹60,000 to ₹1,20,000.

Where should you keep it? A high-interest savings account (some small finance banks offer 6 to 7%) or a liquid mutual fund works well. The key is accessibility — you need to reach this money within 24 to 48 hours, not after a 3-year lock-in.

The most common beginner mistake I’ve seen? Skipping this step entirely because investing feels more exciting. It is more exciting. But so is skydiving without checking your parachute. Build the fund first.

How Much of Your ₹30,000 Salary Should Actually Go Toward Investing?

The 50/30/20 Rule: A Budget That Actually Makes Sense

This framework, popularised by Harvard bankruptcy expert Elizabeth Warren in her book All Your Worth, is simple enough to work and flexible enough to fit most lives:

| Category | Percentage | Monthly Amount (₹30,000) |

|---|---|---|

| Needs (rent, food, utilities) | 50% | ₹15,000 |

| Wants (dining out, entertainment) | 30% | ₹9,000 |

| Savings and Investments | 20% | ₹6,000 |

On a ₹30,000 salary, ₹5,000 to ₹6,000 per month is a realistic, sustainable investment amount.

If you’re lucky enough to live with your parents and your expenses are lower, bump that up to 25 or 30%. The goal isn’t perfection — it’s consistency. Investing ₹3,000 every month without fail is worth infinitely more than investing ₹10,000 twice a year when you remember.

How Much Risk Should You Take?

Here’s a question worth sitting with: how would you feel if your investment portfolio dropped 30% in a single month?

Your honest answer to that question is your risk tolerance. At 25, the beautiful reality is that you have time to recover from market falls. Markets have always recovered — the 2008 financial crisis, the COVID crash of 2020, every major correction in between. What felt devastating in year one often looked like a buying opportunity by year three.

This means you can afford to invest heavily in equity, which historically offers the highest long-term returns. As you get older and take on more financial responsibilities — a home loan, kids, aging parents — you’ll naturally shift toward more stable investments. For now, equity is your friend.

SIPs, Mutual Funds, and Index Funds: What You Actually Need to Know

What Is a SIP, Really?

A Systematic Investment Plan, or SIP, is beautifully simple. You choose an amount — say ₹2,500 — and it automatically gets invested in a mutual fund of your choice every month. No logging in, no deciding when to invest, no market-watching required.

Think of it like a gym subscription that actually makes you fitter. You pay every month. The habit does the work.

The real magic of SIPs lies in something called rupee-cost averaging. When markets are low, your fixed ₹2,500 buys more units. When markets are high, it buys fewer. Over time, your average cost per unit stays lower than if you’d tried to invest a lump sum at the “right” moment. And since nobody — not even professional fund managers — can consistently predict the right moment, the SIP approach takes that guesswork completely off the table.

Index Funds vs Active Mutual Funds: Which Should You Choose?

Both are legitimate. But for someone starting out, understanding the difference matters.

| Feature | Index Funds | Actively Managed Funds |

|---|---|---|

| How it works | Mirrors an index like Nifty 50 | Fund manager selects stocks |

| Cost (expense ratio) | Very low: 0.1 to 0.2% | Higher: 0.5 to 1.5% |

| Performance | Matches the market | May beat or underperform the market |

| Best suited for | Long-term, low-maintenance investors | Those comfortable with active oversight |

Index funds have a quiet superpower: their low cost compounds in your favour over time. A 1% annual fee might sound small, but over 25 years on a growing corpus, that difference can add up to lakhs.

According to SEBI’s own research and global data, a majority of actively managed funds fail to consistently outperform their benchmark index over 10-year periods. That’s not an argument against active funds — some genuinely deliver. But as a beginner with limited time to research fund managers and track records, an index fund gives you solid, predictable exposure to India’s economic growth.

SIPs in Mutual Funds vs Fixed Deposits: The Honest Comparison

| Feature | SIP in Mutual Fund | Fixed Deposit |

|---|---|---|

| Expected returns | 10 to 14% historically | 6 to 7% currently |

| Risk level | Market risk | Near zero |

| Liquidity | Can redeem anytime | Penalty for early withdrawal |

| Beats inflation? | Yes, comfortably | Barely, if at all |

FDs feel safe, and for your emergency fund, they’re fine. But for long-term wealth building? Relying on FDs alone is like filling a bucket with a slow leak. You’re working hard, the money looks stable, but inflation is quietly draining it. According to the RBI’s annual report, household savings in financial assets have been declining as a share of GDP, partly because many Indians still park money in low-yield instruments. Equity investing through SIPs is increasingly being recognized as the better path for long-term retail investors.

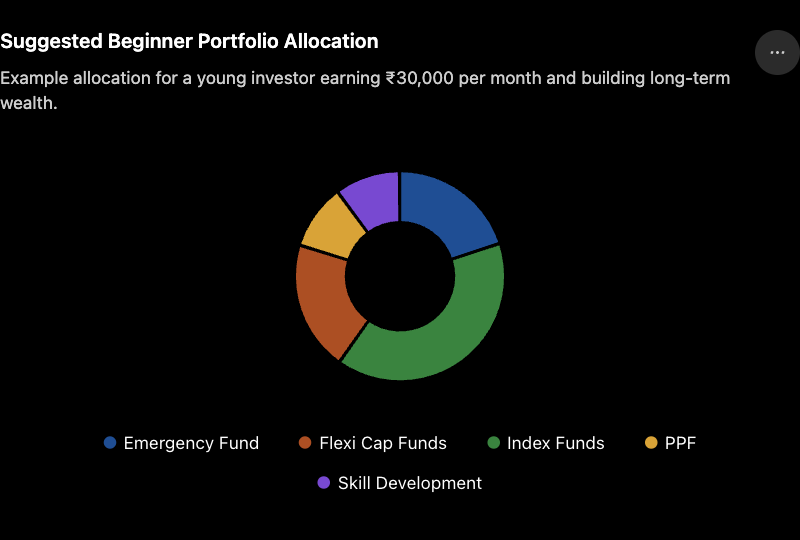

A Practical Portfolio Plan for ₹6,000 Per Month

Here’s a simple, beginner-friendly allocation that balances growth, safety, and tax efficiency:

| Where Your Money Goes | Monthly Amount | Why It’s There |

|---|---|---|

| Emergency Fund (liquid savings) | ₹2,000 until target is reached | Your financial safety net |

| Nifty 50 Index Fund (SIP) | ₹2,500 | Core long-term equity growth |

| Flexi Cap Mutual Fund (SIP) | ₹1,500 | Diversified exposure across market caps |

| PPF (Public Provident Fund) | ₹1,000 | Tax-free returns and retirement foundation |

| Skill Development | ₹500 | Your highest-ROI investment |

The Nifty 50 Index Fund gives you a slice of India’s 50 largest companies — Reliance, TCS, HDFC Bank, Infosys. When India grows, you grow with it. Low cost, low drama, high long-term potential.

The Flexi Cap Fund lets a professional fund manager invest across large, mid, and small companies depending on where they see opportunity. It adds a layer of active diversification without requiring you to do the research yourself.

PPF is a government-backed scheme offering roughly 7.1% per annum, completely tax-free, and your annual investment qualifies for deduction under Section 80C. The 15-year lock-in makes it excellent for retirement investing, because the compounding is uninterrupted. AMFI’s investor education resources have a good breakdown of how PPF works alongside mutual funds.

Skill Development deserves its own line item. A ₹3,000 Coursera certificate or a ₹6,000 professional course can add ₹5,000 to ₹10,000 to your monthly salary within 2 years. The return on investing in yourself often beats the stock market. Don’t skip this.

Asset allocation — the art of spreading your money across different types of investments — is the single biggest driver of long-term returns. Not individual stock picks. Not timing the market. Just having the right mix and leaving it alone.

Mistakes That Will Cost You Years of Growth

Chasing “hot” stock tips. That college WhatsApp group with someone promising 10x returns? The influencer on Instagram showing screenshots of gains? These burn more people than they help. If it sounds too good, it is.

Investing without a goal. “I want to grow wealth” feels purposeful, but gives your money no direction. “I want ₹40 lakh for a home down payment in 8 years” — now that’s a goal. A clear goal determines how much to invest, where to invest it, and when to stop taking risks.

Skipping the emergency fund. Already covered this, but worth saying again: one unexpected expense without a cushion can undo 18 months of SIP discipline.

Waiting for the “right” time to invest. Markets always feel uncertain. There’s always a reason to wait. In hindsight, almost every point in the last 20 years was a good time to start a long-term SIP. Start now.

Stopping your SIP during a crash. A market crash is actually the best time to be running a SIP. Your money buys more units at lower prices. Investors who continued SIPs through the 2020 COVID crash saw significant gains by 2021. The ones who panicked and stopped missed the recovery entirely.

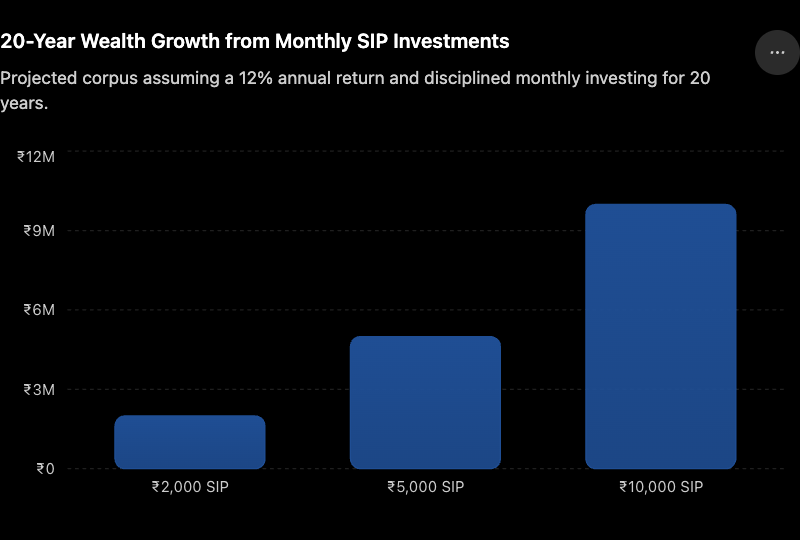

What Does ₹5,000 Per Month Actually Grow Into?

Let’s make this concrete:

| Years Invested | Total You Put In | Estimated Value at 12% p.a. |

|---|---|---|

| 5 years | ₹3,00,000 | ~₹4,12,000 |

| 10 years | ₹6,00,000 | ~₹11,60,000 |

| 20 years | ₹12,00,000 | ~₹49,95,000 |

| 30 years | ₹18,00,000 | ~₹1,76,00,000 |

Look at years 20 to 30. You invested only ₹6 lakh more, but your wealth nearly tripled. That acceleration is compounding, doing its heaviest lifting in the later years. It’s slow at first — almost invisible. Then it becomes astonishing.

Note: 12% is based on historical averages for diversified equity mutual funds in India. Past returns don’t guarantee future results, and actual returns will vary.

What a Legend of Investing Would Tell You

John Bogle, the man who invented the index fund and founded Vanguard, spent his life telling individual investors one thing:

“Don’t look for the needle in the haystack. Just buy the haystack.”

He meant: stop trying to find the perfect stock, the perfect fund, the perfect entry point. Just buy a broad market index fund, keep buying every month, and let India’s economic growth work for you over decades.

This philosophy is exactly what sits behind AMFI’s “Mutual Funds Sahi Hai” campaign and SEBI’s push for greater retail participation in equities. SEBI’s Investor Education portal offers free, unbiased guidance on understanding mutual funds, index funds, and risk — worth bookmarking if you want to go deeper.

Frequently Asked Questions

Is ₹30,000 salary enough to start investing?

More than enough. Investing isn’t about income level — it’s about consistency. Even ₹3,000 to ₹5,000 per month started in your mid-20s, invested through SIPs in diversified mutual funds, can build substantial long-term wealth through compounding. The income level matters far less than starting early.

How much should I invest from a ₹30,000 salary?

A good target is 20% of your income, which works out to ₹6,000 per month using the 50/30/20 budgeting framework. If you live with family and have lower expenses, push it to 25 to 30%. Start by securing your emergency fund, then direct the rest into SIPs.

Which SIP is best for beginners?

A Nifty 50 Index Fund SIP is the most beginner-friendly starting point. It’s low-cost (expense ratios as low as 0.1%), diversified, and tracks India’s 50 largest companies. Fund houses like UTI, Nippon India, HDFC, and SBI offer well-regarded options. Always compare expense ratios before choosing.

Should I save first or invest first?

Both, in order. First, build an emergency fund covering 3 to 6 months of expenses in a liquid, accessible account. Then start investing. Jumping straight to investments without a safety net means you risk withdrawing early during a crisis, often at a loss.

Can I become wealthy by investing just ₹5,000 per month?

Yes, with patience and time. At a 12% average annual return, ₹5,000 per month grows to roughly ₹1.76 crore over 30 years — from a total personal investment of just ₹18 lakh. Consistent, long-term SIP investing has made ordinary salaried professionals genuinely wealthy in India.

What’s the safest investment option for young professionals?

PPF is the safest structured investment available to Indian retail investors — government-backed, tax-free returns of around 7.1% per annum, and eligible for 80C deductions. For better long-term growth with moderate risk, a combination of PPF and a Nifty 50 index fund covers both safety and upside.

The Most Important Step Is the First One

You don’t need to have everything figured out. You don’t need a financial planner, a trading terminal, or a high salary. You need to start.

Open a savings account and start building your emergency fund this month. If you’re unsure how much to keep aside, use our emergency fund calculator India guide to figure out the right amount. Pick a SEBI-registered investment platform like Groww, Kuvera, or Zerodha Coin and set up a SIP of even ₹2,000 in a Nifty 50 index fund. Open a PPF account at your nearest bank or post office. Then automate everything so the money moves before you can spend it.

Investing at 25 on a ₹30,000 salary is not about getting rich quickly. It’s about building something quietly, steadily, over the years — until one day the numbers surprise even you. Small amounts. Long time horizons. Boring consistency.

That’s the whole plan. And it works.

Your future self is counting on the decision you make today.

About the Authors & Contributors

Written by: Bryson Finley

Published by: Daniel Sams

Bryson Finley is the Co-founder of pantheonuk.org and Getapkmarkets.com. As a leader in the digital and tech space, Bryson specialises in providing the analytical foundations necessary for young professionals to leverage modern tools for long-term financial growth and investment success.

{kind=link}